Tuesday, August 29, 2006

Reflate or Deflate: the FED's Options Look Ugly

EUR/USD 1.2810 Hi 1.2840 Low 1.2776

USD/JPY 116.74 Hi 117.27 Low 116.57

AUD/USD 0.7621 Hi 0.7634 Low 0.7583

EUR/JPY 149.51 Hi 150.08 Low 149.47

Right now the "idiot savant" that is the Financial Markets is concerned with only one question: is the FED done? Around this little question fortunes are being bet. The idea is that the FED controls everything: the performance of the USD, the Stock Market, the United States Economy and the fortunes of our political masters. It's a nice idea. And it's simple so we can all focus on the data with the aim of guessing the FED's next move. But things are just slightly more complicated than that.

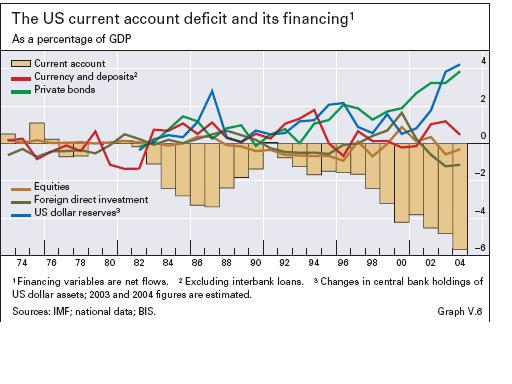

What we know is this: Anglo-Saxon economies are drowning in debt. This debt, given the paucity of domestic savings in these economies, has been largely financed by inflows of foreign capital. The aftermath of the Asian Crisis (1997-1999) facilitated these inflows. The Asian Crisis started in currency markets. Massive devaluations following ill-advised comments by the IMF official, Michel Camdessus, saw contagion and caused financial dislocation and real economic distress in emerging economies in Asia. For our purposes, however, what happened to the economies in Asia is irrelevant. What is relevant is that subsequent to the Asian crisis there was the huge drive by Asian Emerging Economies to accumulate sufficient foreign currency reserves to avoid any future currency crisis. That is: Asian Central Banks bought massive amounts of foreign currency, mostly USDs. This allowed the United States to run up an enormous external deficit and finance a massive domestic debt binge without the USD suffering and without a corresponding rise in domestic interest rates. It also allowed U.S. Officials to become nonchalant about the USD and debt financing in general: rates were low, credit was easy. Both the Public and Private sectors in the States have accumulated massive levels of debt which have financed speculative bubbles in the Stock Market, the Housing Market and allowed the Consumer and the Federal Government under Bush to go on huge spending sprees: the Iraqi War being a case in point. There are not expected to be any positive returns from the Consumer Debt binge or the War Effort, these are not investment propositions. After the event all that is left is the debt.

There are two possible solutions: the U.S. can attempt to reflate it's way out of the problem This would allow today's debt to become irrelevant in tomorrow's money. Essentially reflation means that the guy who lent you the money loses. To reflate the FED would need to stand pat or even EASE. Inflation would be allowed to re-emerge. It would also mean allowing the USD to devalue, perhaps abruptly. This would likely see foreign capital inflows slow or stop. Refinancing existing debt would become more expensive and, with the FED standing pat, the yield curve would move from its current negative slope to steep positive slope. This appears to be the FED's chosen option. It is not without risks to domestic financial markets and the real economy. Just remember what happened to Asia, which was flavour of the month with investors, before massive currency devaluations occurred.

The alternative would involve holding the USD close to current exchange rates and fighting inflation with steady or higher domestic interest rates. The yield curve would continue remain negative. In this way debt would financed via decreased levels of domestic consumption and/or a sharp reduction in the FEDERAL Government deficit. Retiring debt would require even greater economic retrenchment. Either way there would be a recession. And it could be severe. The result of this policy option would be: DEFLATION and an economic recovery which would be very much delayed. Think Japan in the 1990s and you get the general idea.

Right now there is no happy policy route for the FED. Bernanke the mild, however, seems inclined to REFLATE and be damned.

Financial Market Outlook

The USD has failed to rally, despite the reasonably positive performance of the U.S. Stock Market yesterday. While the market will continue to focus on the numbers, unless a very compelling NEW REASON to buy the USD emerges in the short term, the medium term risk for the USD remains to the downside. Prudence suggests: sell on rallies.

Oil 70.80

Gold 626.00

For now all quiet (well it's all relative) in the Middle East has seen the price of OIL retrace slightly.

Weak economic data out of the States, which remains the world's largest OIL importer, can be expected to see prices contained on the upside. Simmering GEOPOLITICAL tensions, however, suggest that the downside is also limited. For now we have range trading. The market needs new information.

USD/JPY 116.74 Hi 117.27 Low 116.57

AUD/USD 0.7621 Hi 0.7634 Low 0.7583

EUR/JPY 149.51 Hi 150.08 Low 149.47

Right now the "idiot savant" that is the Financial Markets is concerned with only one question: is the FED done? Around this little question fortunes are being bet. The idea is that the FED controls everything: the performance of the USD, the Stock Market, the United States Economy and the fortunes of our political masters. It's a nice idea. And it's simple so we can all focus on the data with the aim of guessing the FED's next move. But things are just slightly more complicated than that.

What we know is this: Anglo-Saxon economies are drowning in debt. This debt, given the paucity of domestic savings in these economies, has been largely financed by inflows of foreign capital. The aftermath of the Asian Crisis (1997-1999) facilitated these inflows. The Asian Crisis started in currency markets. Massive devaluations following ill-advised comments by the IMF official, Michel Camdessus, saw contagion and caused financial dislocation and real economic distress in emerging economies in Asia. For our purposes, however, what happened to the economies in Asia is irrelevant. What is relevant is that subsequent to the Asian crisis there was the huge drive by Asian Emerging Economies to accumulate sufficient foreign currency reserves to avoid any future currency crisis. That is: Asian Central Banks bought massive amounts of foreign currency, mostly USDs. This allowed the United States to run up an enormous external deficit and finance a massive domestic debt binge without the USD suffering and without a corresponding rise in domestic interest rates. It also allowed U.S. Officials to become nonchalant about the USD and debt financing in general: rates were low, credit was easy. Both the Public and Private sectors in the States have accumulated massive levels of debt which have financed speculative bubbles in the Stock Market, the Housing Market and allowed the Consumer and the Federal Government under Bush to go on huge spending sprees: the Iraqi War being a case in point. There are not expected to be any positive returns from the Consumer Debt binge or the War Effort, these are not investment propositions. After the event all that is left is the debt.

{kind=link}

There are two possible solutions: the U.S. can attempt to reflate it's way out of the problem This would allow today's debt to become irrelevant in tomorrow's money. Essentially reflation means that the guy who lent you the money loses. To reflate the FED would need to stand pat or even EASE. Inflation would be allowed to re-emerge. It would also mean allowing the USD to devalue, perhaps abruptly. This would likely see foreign capital inflows slow or stop. Refinancing existing debt would become more expensive and, with the FED standing pat, the yield curve would move from its current negative slope to steep positive slope. This appears to be the FED's chosen option. It is not without risks to domestic financial markets and the real economy. Just remember what happened to Asia, which was flavour of the month with investors, before massive currency devaluations occurred.

The alternative would involve holding the USD close to current exchange rates and fighting inflation with steady or higher domestic interest rates. The yield curve would continue remain negative. In this way debt would financed via decreased levels of domestic consumption and/or a sharp reduction in the FEDERAL Government deficit. Retiring debt would require even greater economic retrenchment. Either way there would be a recession. And it could be severe. The result of this policy option would be: DEFLATION and an economic recovery which would be very much delayed. Think Japan in the 1990s and you get the general idea.

Right now there is no happy policy route for the FED. Bernanke the mild, however, seems inclined to REFLATE and be damned.

Financial Market Outlook

The USD has failed to rally, despite the reasonably positive performance of the U.S. Stock Market yesterday. While the market will continue to focus on the numbers, unless a very compelling NEW REASON to buy the USD emerges in the short term, the medium term risk for the USD remains to the downside. Prudence suggests: sell on rallies.

Oil 70.80

Gold 626.00

For now all quiet (well it's all relative) in the Middle East has seen the price of OIL retrace slightly.

Weak economic data out of the States, which remains the world's largest OIL importer, can be expected to see prices contained on the upside. Simmering GEOPOLITICAL tensions, however, suggest that the downside is also limited. For now we have range trading. The market needs new information.

![]()